The currency board is the most suitable money restriction until the acceptance of the EURO

Recently people started talking again about the currency board. This time around the discussion was started not by Bulgarian analysts but foreign experts. In their opinion representatives of the European Central Bank claim, that the countries which have accepted the currency board will have problems to maintain good results over sufficiently long time. They face the challenge to be stable in the process of convergence to the average levels of income in the European Union.

The key aspects of economic freedom are several – voluntary exchange, low taxes and prudent fiscal policy, protection of property right, stable currency, limited interference of the state with the economy, free movement of capitals, market definition of wages and prices. In Bulgaria the way to achieve stability of the currency was through the introduction of the currency board. The meaning of the board is that the Bulgarian Central Bank is strongly restricted to lead an independent monetary policy. The Bulgarian lev is linked to the euro by a strictly defined exchange rate, assuming that this anchor will insure low levels of inflation. The Bulgarian National Bank does not control the interest rates in the country (it announces the base interest rate, but does not determine it), does not perform open market operations (purchases and sales of government bonds for its own account), as it does not have the right to credit the government under any form; does not buy discounted policies from commercial banks, thus providing credits to the commercial bank only in case of systematic liquidity crisis and then it is guaranteed by marketed securities. The only instrument of monetary policy, which BNB is allowed to use is the minimum required reserves. The aim is however that the level of these minimal required reserves should reach the average levels in the EU – approximately 2% of depository base.

All measures mentioned above are aimed at applying strict budgetary restrictions on the entire country, which leads to the necessity the government to maintain close to balanced budgets. This refers to the private sector as well – commercial banks could not expect from the central bank to save them if they carry unwise policies. They must limit the risk in their operations which they perform – for example crediting. The situation is identical in the real sector – the repetition of the situation from 1996-7 is not possible. At that time the loss making state companies were accumulating debts, which at the end of the day were covered by local currency emissions. The moral hazard was extremely high, since the managers of these companies and of the entire public sector knew that the expenditures which they make will afterwards be covered. Thus we got an uncontrolled increase of borrowing. The decision of the government at that time was to devalue the currency in order to reduce the real value of those debts. This however meant, that the creditors (in that case almost the entire population) lost by the devaluation of the lev, while the wealth was redistributed towards the borrowers but in addition the uncertainty increased and real incomes were reduced.

All of this resulted from the unstable currency. The currency board stabilized the lev against the euro (initially against the German Mark) and hence against the main global currencies. The Board reduced the inflationary expectations in the country, since specifically the exchange rate was used as the "price" of the money during the crisis. The economy was gradually stabilized, the confidence in the lev increased, the level of substitution of the local currency by foreign currency was reduced and the real incomes began to increase. Naturally the stable lev is not the only reason for the positive developments. Very significant is the effect from withdrawal of the government from the economy through privatization and the reduced control of wages and prices, liberalization of capitals, reduced obstacles to international trade. The currency board however represents one of the fastest and complete reforms which results are easy to note. The reduction of the inflation rate after 1997 is drastic compared to the one before that. The financial stability significantly increases the possibilities for effective direction of the savings into productive investments, which at the end increase the economic growth.

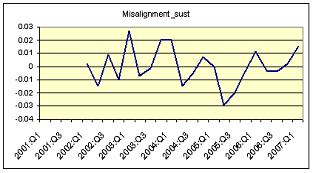

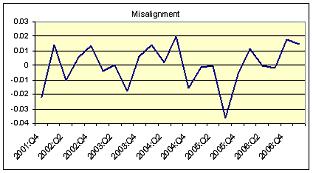

Naturally, the currency board has its opponents, which claim that the higher inflation rates in the country lead to overvaluing of the lev as compared to the fixed exchange rate. These statements however are unfounded and represent an arbitrary claim. In this case it is necessary to differentiate between two different concepts. The real appreciation of the lev is a result of the inflationary differential with the main commercial partners. The over valuation, however is linked to the comparison between the current exchange rate and the equilibrium exchange rate defined by the fundamental factors. Only such a comparison could show whether or not the lev is overvalued. To this aim it is necessary to develop a model with which to find the equilibrium value of the lev. The factors which determine the equilibrium rate are the terms for trade (i.e. the relative prices between the exported and imported goods), the gross savings and the foreign direct investments. Their interactions lead to the increase of the equilibrium rate. The results from the model are shown on Figures 1 and 2, which represent the short term and medium term differences between the current value of the lev and the equilibrium determined by the fundamental factors. Along the Y axis is the difference in percentages, while along the X axis is the respective quarter. As a whole the difference between the real value and the calculated value is within the range of +/- 4 per cent during the period between the introduction of the currency board and the first quarter of 2007. Hence, it is not appropriate to state that the lev is over valued, which means that the fixed exchange rate must be kept at the current level. Besides that, the conversion after the euro becomes the official means of payment must be done at that rate.

Figure 1: Short term misalignment (between the current REER and estimated equilibrium REER)

Figure 2: Sustainable misalignment (between the current REER and estimated medium term equilibrium REER)