Public Expenditures – A Feast in Times of Crisis

We would like to pay attention to the latest data on employment and salaries in the late 2009, which shows some disturbing public sector tendencies, especially in the public administration.

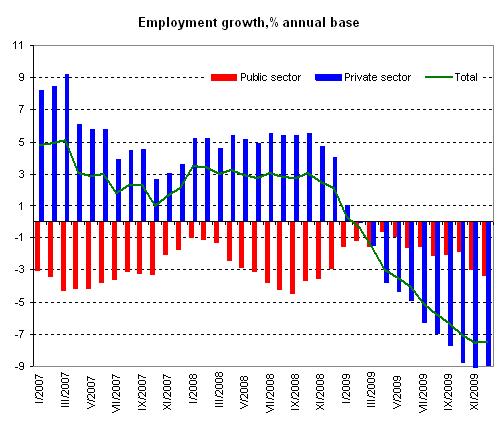

According to the national statistics’ data, the economy employment marks a 7,5% drop in December in comparison with the year before which is a normal tendency during a crisis. Somewhat encouraging is the interruption of the accelerating falling trend. The annual reduction is remaining at the level of the previous month.

As might be expected, employment by different economic sectors shows greater personnel reductions in the most crisis-affected sectors in Bulgaria. For example the manufacturing industry which is the greatest employer in the economy has a double digit reduction in the second half of the year, which reaches 12% for December on an annual base. Reduction in construction reached 33.3% annually in December (15.3% average annual), the number of employed shrinked dramatically too – 18.1% in December 2009. Tourism, financial sector and real estate brokerage are the other sectors experiencing serious personnel reduction due to low activity.

Source: National Statistics Institute, IME calculations

What is striking is the significantly slower employment reduction in the public sector compared to the private. While we have 8.9% employment reduction in December in the private sector, in the public sector it is only 3.3% for the same period. Nevertheless, we have to admit that more serious reduction of the employed is observed from August onward, i.e. since the new government came in office. Till the end of December the employed there have been reduced by 6.8% annually. It is a different issue to what extent employees are discharged or vacant jobs have been closed as is traditionally done when an administration reduction initiative is carried out.

The upper graph shows that the private sector employment is moving together with economic activity, and the reactions of the labor market follow the business environment with a traditional lag of about a year. Since the beginning of 2009 accelerating drop in the private sector employment is observed. We observe an accelerating drop in private sector employment since the beginning of 2009. Even if the real sector starts to recover as forecasted, the reduction will most probably continue throughout 2010 due to delayed reaction of the labor market.

At the same time public employment dynamics show little to no connection with the economy condition. As in 2007 (a high growth year), the last two years score between 1 and 4% employment reduction in the public sector annually without any connection to the economic situation. Public sector personnel has been reduced by barely 6% for the last three years and by even less in the administration (4.7%). The real personnel reduction is even less if closed job vacancies are taken into account.

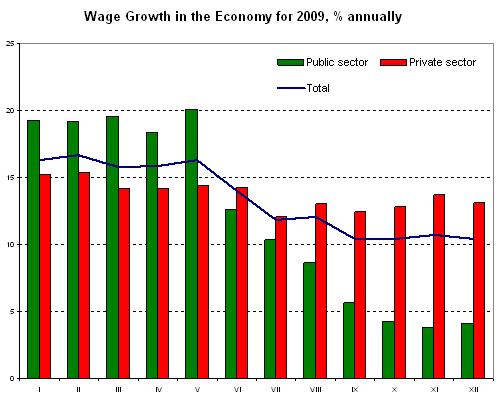

Amid these tendencies it would be interesting to look at salaries in the economy. The salary dynamics in 2009 de facto illustrate the Dornbusch Sticky Price Model which considers prices and salaries hard to adjust in short term, especially when descending.

Source: National Statistics Institute, IME calculations

In spite of the serious difficulties the national economy faced in 2009 and the mentioned personnel reduction, salaries kept growing last year. Despite a slowdown in the second half, the growth stayed well over 10% annually [1]. It is interesting that the private sector salaries, that should be reacting to the crisis more quickly and strongly, remain relatively stable. This could be explained by the general practice of officially declaring the required professional minimum for insurance contributions and not the whole salary. I.e. if the salary is de facto reduced as predicted, it is not reflected by the national statistics. At the same time the public sector salaries score a slowing growth in 2009.

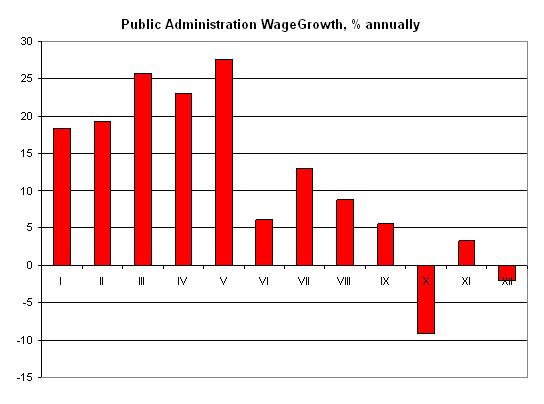

Especially interesting is the situation with the public administration. The salary growth in the first months of the year reached double digit numbers despite the lack of official salary increase in the budget sector. Actually the salary growth in the second half of the year shrank but stayed positive excluding October and November.

Source: National Statistics Institute, IME calculations

Especially interesting are the remunerations in the public sector in general and the government in particular. The annual private sector remunerations were 3.6% from the average fourth quarter salary and those in the public sector were 6.1%. Despite the 50% public sector remuneration drop in absolute value, their percentage salary share is significantly higher than the private one. Even more striking is the situation in the public administration. Their annual remuneration has reached 10.7% from the salaries in the last quarter. The presence of serious remunerations contradicts the budget sector bonus and pay ban repeatedly announced by the finance minister in 2009. It turns out there have been substantial remunerations despite the ban. Not to mention that some of the payments in the administration are classified as extra payment for certain functions which is not registered in the official statistics and it is possible that higher real remunerations were paid.

Taking everything into account it is obvious why budget salary and remuneration expenditure scored a real growth during a crisis year (see here) despite the serious budget revenue contraction. In this respect we hope the announced administration pay reform which is to start in 2011 to be accompanied by overall administrative maintenance reduction. The declared increase in the permanent part of the salary in the administration, as well as the parallel minimum and maximum profession pay level increase however makes the impression that this reform could again end up with higher administrative expenditure on behalf of all of us, the taxpayers.

[1] Salary growth is in nominal values due to low 2009 inflation (2.8% average annual and 0.6% in December, annual base) which presumes close real change value.